-

Home

-

News

- Latest News

Latest News

- Details

- Hits: 1513

Acres team are set, and ready for this years fun run on Sunday.

Please come along and support all the runners, walkers and teams. It is a great day, superb atmosphere and best of all - thousands of pounds will be raised for many deserving charities - Course route

Acres are proud to once more be supporting MDNA- Donate here

- Details

- Hits: 5838

When considering the factors that influence house prices, schools often emerge as a key player in the equation. The proximity and quality of schools have a significant impact on the desirability of a neighbourhood, which, in turn, affects property values. This blog will delve into the intricate relationship between schools and house prices, exploring how educational institutions can cause a ripple effect that shapes the local property market.

The Educational Ecosystem and Property Values

For families, the quality of education a school provides is a top priority. As parents seek to secure the best possible educational opportunities for their children, they are willing to invest in homes located in areas with reputable schools. Thus, a symbiotic relationship between schools and property values is established. Here’s how it works:

- Demand and Attraction: High-performing schools create a surge in demand for homes within their catchment areas. Families often move or relocate to these areas to ensure their children receive a quality education. This increased demand leads to competition among buyers, ultimately driving up property prices. In 2019 PriceWaterhouseCoopers (PWC) reported that on average house prices near a top primary school costs £27,000 more than in a wider area, and £25,000 more near the top 10 % of secondary schools. Living close to one of England’s top primary and secondary state schools can add over £25,000 to the price of a house (pwc.co.uk )

- Resale Value: Homes situated near well-regarded schools tend to hold their value better over time. Even during economic downturns, these properties remain sought after, shielding homeowners from steep value declines. You can monitor house prices by seeing what homes have sold for in your area. Sold House Prices | See UK House Prices Online | Rightmove

- Homebuyer Psychology: The mere presence of a renowned school can enhance the perceived desirability of an area. The prestige associated with such institutions contributes to a positive image of the community, further boosting property values. The Department of Education published a report in 2017 which analysed 3 years of house price data and concluded “The value of houses near the poorest- performing schools are also lower than in the surrounding areas. House prices near the 10% best-performing primary schools are 8.0% higher than in the surrounding area.” The report can be found here School performance and house prices: analysis – GOV.UK (www.gov.uk)

The Catchment Area Effect

One of the most prominent ways schools influence house prices is through catchment areas. A catchment area refers to the geographical boundary within which a particular school has priority for student enrolment. As the quality of a school improves, homes within its catchment area become particularly attractive to families.

- Catchment Area Premium: Properties within a high-performing school’s catchment area often command a premium compared to those outside the boundary. This premium can be substantial and may vary depending on the school’s reputation and the scarcity of available homes.

- Competition and Bidding Wars: Limited supply coupled with high demand within a catchment area can lead to bidding wars among prospective buyers. In such scenarios, home prices can skyrocket well above the original listing price.

Investment in Infrastructure

Council investments in school infrastructure can also impact local housing markets. When educational institutions receive funding for improvements, expansions, or modernisation, it not only enhances the learning environment but also contributes to the overall appeal of the surrounding community area.

- Infrastructure Upgrades: Modern school buildings, state-of-the-art facilities, and advanced technology attract families seeking a contemporary and conducive learning environment for their children. These upgrades can indirectly contribute to a rise in property values.

- Local Area Transformation: School improvements often spill over into the community, leading to a positive transformation of the local area. This can include better roads, increased safety measures, and improved public spaces—all of which contribute to heightened desirability and subsequent property value appreciation.

The relationship between schools and house prices is intricate and multifaceted. The quality of education provided by a school and its catchment area can significantly influence the demand for homes and impact property values. As families prioritise access to reputable educational institutions, the housing market responds with increased demand and higher prices. Additionally, investments in school infrastructure can catalyse neighbourhood improvements that further boost property values.

For homeowners and prospective buyers alike, understanding the dynamics between schools and house prices is essential for making informed decisions. As communities continue to evolve, the ripple effect created by schools will continue to play a pivotal role in shaping local housing markets.

Want to check how much your home is worth? You can get an Instant Valuation here.

If you would like to discuss selling your home, please get in touch with us This email address is being protected from spambots. You need JavaScript enabled to view it. or call any of our busy, helpful teams/offices:

Four Oaks 0121 323 3088

Sutton Coldfield 0121 321 2101

Walmley 0121 313 2888

Great Barr 0121 358 6222

Lettings 0121 312 4997

Mortgages 0121 387 1616

Thank you for reading this article, and your interest in Acres and our property for sale.

Nigel & Jayne Deekes – Acres Partners

- Details

- Hits: 1525

House prices show growth year on year

Key takeaways: April 2025 House Prices

- House prices in the West Midlands rise : 2.3% year on year ( Zoopla April 25 ) & by 1% ( Rightmove April 25 ) the average asking price of home hits a new record, at just over £261,316

- Our snapshot of the housing market after stamp duty increase suggests people are carrying on with their home moves

- New home-buyer demand is up 5% compared to last year, with new sellers coming to market up by 4% ( Rightmove April 25 )

- Mortgage rates may drop more quickly than anticipated if the Bank of England reduces the Base Rate in May

As the days get longer, Spring is in full bloom and the weather improves so does the property market, with more home-movers springing into action. This year, we’ve seen some more substancial changes in the market than usual, with for example the temporary stamp duty holiday ending from the start of April.

But the latest snapshots of the housing market shows that most people are moving on as normal, indeed this first quarter, here at Acres we have been pleasantly surprised, and very pleased by the levels of Sales and New Instruction coming to market with sales to the end of March, our year end, being 41% higher than the previous year, listings 18% higher, and properties completed once more 41% higher, a great year.

You can check the average prices in the region by viewing Rightmove’s House Price Index report for April and also the latest sold prices in your area here.

What is the reason for price increases ?

Traditionally we see increases in the Spring, when the housing market is at its busiest. However, this month’s jump is bigger than the usual price rise we see in April.

This is because demand from those looking to buy a home is up by 5% compared to this time last year, while the number of new sellers coming to market has also increased by 4%. ( data from Rightmove )

Nigel Deekes – founding Partner of Acres comments : “ It has been an exceptionally busy 12 months, the market has moved forward, as have Acres, once more proportionally taking more New instruction and Sales from the stock of property in the area. We’ve seen our prices move forward marginally, and the anticipated slow down from the withdrawal of the stamp duty savings impacting the market less than expected, as the general additional £2,500 payable perhaps not being as big a deterrent as expected, given the average price of a property in the area the stamp duty increase proportionally has less impact and desire for many to move remains strong, life goes on. “

Chris Deekes - Associate Partner, and managers of Acres Great Barr " Since the recent stamp duty changes, we haven’t seen an increase in the number of home sales falling through, which indicates there hasn’t been a backtracking from buyers who were unable to complete before the tax rise. There was also a significant rush to complete sales before the April deadline."

With more homes available for sale than at this time last year, there’s more competition, so it’s really important if you’re thinking of selling your home to work with your agent to get the price right.

Chris Harvey Managers of Acres Four Oaks explains: “March was a very busy month, with significantly more completions than usual. We, and solicitors worked very hard to get so many sales through. April has started off as a busy month, with instructions up, as are viewings and offers across all of four North Birmingham offices.”

What’s happening with mortgage rates?

Rightmove analysis shows Average mortgage rates remain just below 5%, with the current average five-year fixed mortgage rate of 4.72% being only slightly lower than this time last year. If the Bank of England opts for further and faster rate cuts, starting in May, then mortgage rates could drop more quickly than anticipated. You can check the current average mortgage rates here.

Know your mortgage bughet in 2 minutes :

- Discover your maximum borrowing power https://acres-fs.co.uk/aea-mortgage-borrow-calculator

- Establish your monthly repayments https://acres-fs.co.uk/aea-mortgage-repayment-calculator

- See homes you know you can afford www.acres.co.uk

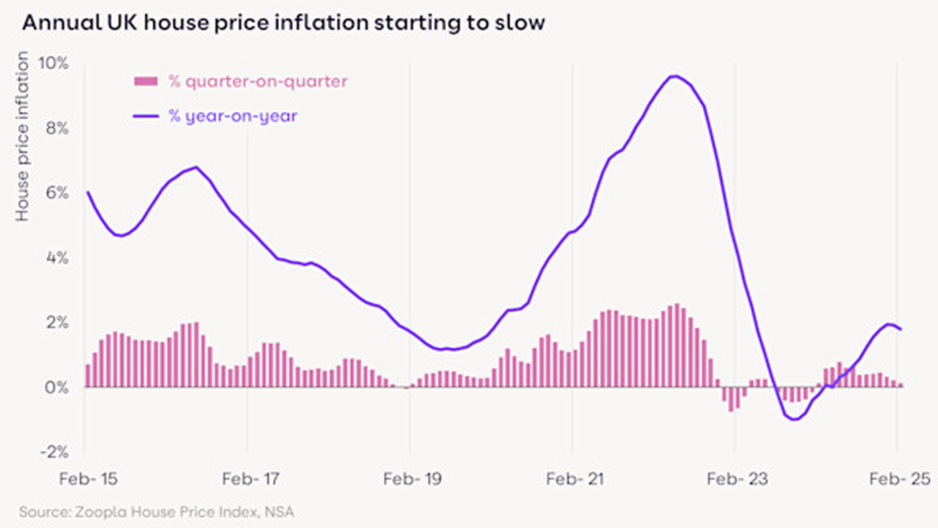

House price inflation slows as supply grows

House price inflation is still relatively slow after a good recovery over the last 12 months. The annual rate of UK house price inflation edged lower in February to 1.8%.

Prices are still rising faster than a year ago (-0.2%) but we expect the rate of UK house price inflation to moderate in the coming months. ( Data from Zoopla )

There are several factors behind the expected slowdown. The number of homes for sale is growing faster than the number of sales being agreed, boosting choice for buyers and re-enforcing a buyers’ market.

While house price inflation is slowing, the number of sales agreed continues to increase, up 5% on a year ago, with demand 10% higher.

Lettings News

Annabelle Reynolds, Acres lettings manager comments : “ In March 2025, the UK's residential rental market is experiencing significant growth, with rental prices expected to increase considerably. This growth is projected to continue through 2029, with a cumulative increase of nearly 18%. Specifically, the UK rental market is poised for a surge, with a robust eight percent rise anticipated in 2024. Additionally, the {"How to Rent" guide https://www.mydeposits.co.uk/content-hub/how-to-rent-guide/} is a crucial resource for landlords, outlining the legal requirements for renting out properties. Landlords must ensure their properties are in compliance with the latest version of the guide, which includes providing adequate insurance, checking smoke and carbon monoxide alarms, and ensuring valid gas safety certificates, EICRs, and EPC"

Want to check how much your home is worth? You can get an Instant Valuation here.

If you would like to discuss selling your home, please get in touch with us This email address is being protected from spambots. You need JavaScript enabled to view it. or call any of our busy, helpful teams/offices:

Four Oaks 0121 323 3088

Sutton Coldfield 0121 321 2101

Walmley 0121 313 2888

Great Barr 0121 358 6222

Lettings 0121 312 4997

Mortgages 0121 387 1616

Thank you for reading this article, and your interest in Acres and our property for sale.

Nigel & Jayne Deekes – Acres Partners

- Details

- Hits: 3108

Did you know that Spring tends to be the best time to sell a property? It’s true – the Spring months of March to May are arguably the best and most consistent months for property sales year in, year out. Whether you’re an investor or homeowner looking to sell your property, here are the top five reasons why SPRING is the best time of year to get your property on the market and ready to sell.

1. High level of demand and need for supply

The warmer Spring months with lighter, brighter days tend to be more appealing for property hunting than the heat of the Summer or the freezing cold of the Winter. With an increase in demand for properties, it makes sense for sellers to take advantage of the selling opportunities and put a property on the market.

2. It’s the season of new beginnings

Spring is typically a season associated with new beginnings – you’ll see new buds appearing on trees, new flowers emerging from ground and new life in nature – and this feeling of newness seems to flow through to the property market too. It’s a time when people begin to think about new possibilities and make plans for the rest of the year, such as buying a new property and moving house.

3. Spring weather boosts kerb appeal

The lighter, brighter days of spring can significantly help to boost the kerb appeal of properties. The days tend not to be as dark and dreary as they can be during the heart of winter (bar the occasional weather decline!) and better natural light helps improve the exterior view of properties. For example, it can bring out the natural colour of stone or bricks or make architectural features look better.

Even if you don’t have a property with a garden, there’s likely to be trees coming into bloom or flowers blossoming in your neighbourhood, which can reflect positively on your property too. If you have an apartment with a balcony, a few pots of pretty Spring flowers could brighten up the outdoor space and add an inviting appeal.

4.Spring light aids interior photography

In the same way that improved natural light aids exterior kerb appeal, so too will it help aid the interior photography of your property. Good photos are a key element of successfully selling your property and it definitely makes a difference when there’s better natural light in which to take them. They’ll be less time-consuming editing involved to get them up to scratch and, in theory, it could be quicker for your agent to get your property listed.

5. It’s better weather for moving

On a practical note, for those that are thinking of moving, Spring is a more appealing time to do so. The weather tends to be better than during the Winter and you’re not yet thwarted by the energy-zapping heat that Summer can bring. Plus, for families with children, it’s likely to be an easier time of year to move, whilst they’re still at school and so they can be settled in a new home before a new school year starts in September.

If you need any help, or advice on your purchase and of course mortgages we here at Acres can help, Click here to use our multiple mortgage and stamp duty calculators

If you’re thinking of selling your property to take advantage of the Spring boost in sales, don’t forget to get your property looking its best first. A good spring clean can freshen up your interior and a quick lick of fresh paint on your front door can make the world of difference and improve the look and feel of your property – those first impressions really count! Contact us today to get your property on the market now

Want to check how much your home is worth? You can get an Instant Valuation here.

If you would like to discuss selling your home, please get in touch with us This email address is being protected from spambots. You need JavaScript enabled to view it. or call any of our busy, helpful teams/offices:

Four Oaks 0121 323 3088

Sutton Coldfield 0121 321 2101

Walmley 0121 313 2888

Great Barr 0121 358 6222

Lettings 0121 312 4997

Mortgages 0121 387 1616

Thank you for reading this article, and your interest in Acres and our property for sale.

Nigel & Jayne Deekes – Acres Partners

- Details

- Hits: 4321

The Benefits of Using a Mortgage Broker/Advisor.

Are you considering buying a home or remortgaging and need to secure a mortgage?

One crucial decision you'll face is whether to use a mortgage broker. While some may opt for going directly to a bank or lender, there are significant advantages to working with a mortgage broker.

Here are some key benefits:

* Access to a Wide Range of Lenders*

Mortgage brokers have access to a wide range of lenders. This means they can help you compare offerings from various lenders, including banks and specialist lenders.

*Tailored Solutions*

Every individual's financial situation is unique. A broker can tailor mortgage solutions to your specific needs and circumstances. Whether you're a first-time buyer, self-employed, or have a complex financial situation, a broker can find a mortgage product that suits you.

*Saves Time and Effort*

Searching for the right mortgage can be time-consuming and overwhelming, especially if you're unfamiliar with the mortgage market. A broker can streamline the process by doing the legwork for you, saving you time and effort.

*Expert Advice and Guidance*

Mortgage brokers are experts in their field. They can offer valuable advice and guidance throughout the mortgage application process, helping you understand the terms and conditions of different mortgage products and guiding you through the paperwork.

*Potential Cost Savings*

By accessing a wide range of mortgage products, brokers can often find deals with lower interest rates and better terms than those available through individual lenders. This can result in significant cost savings over the life of your mortgage.

In conclusion, using a mortgage broker can provide you with a range of benefits, including access to a wide variety of lenders and products, tailored solutions, time and effort savings, expert advice, and potential cost savings. So, when you're ready to buy a home, consider enlisting the help of a mortgage broker to guide you through the process and help you secure the best possible mortgage deal.

Contact our dedicated, helpful, knowledgeable team for further help and information

Lisa or Rahma : 0121 358 6222

See our extensive range of mortgage and loan calculators here : https://acres-fs.co.uk/

Your home may be repossessed if you do not keep up repayments on your mortgage

Want to check how much your home is worth? You can get an Instant Valuation here.

If you would like to discuss selling your home, please get in touch with us This email address is being protected from spambots. You need JavaScript enabled to view it. or call any of our busy, helpful teams/offices:

Four Oaks 0121 323 3088

Sutton Coldfield 0121 321 2101

Walmley 0121 313 2888

Great Barr 0121 358 6222

Lettings 0121 312 4997

Mortgages 0121 387 1616

Thank you for reading this article, and your interest in Acres and our property for sale.

Nigel & Jayne Deekes – Acres Partners